Independent sponsor investing gives accredited investors deal-by-deal access to established, cash-flowing businesses in the lower middle market, without committing capital to a blind pool. It is one of the more compelling corners of private markets, but historically one of the hardest to access without the right relationships.

The most accessible way to invest in independent sponsor deals today is through a co-investment platform like CapitalPad, which provides curated deal flow from independent sponsors with investment minimums as low as $25K per deal. For investors with larger individual check sizes ($500k+) and established networks, family office connections and direct sponsor relationships offer additional channels and additional sources of attractive deal flow, but for many accredited investors entering the asset class, a co-investment platform is the practical starting point.

This guide covers how independent sponsor deals work, what returns investors can expect, and how to evaluate the best access channel for your situation.

Key Takeaways

- Independent sponsors acquire businesses deal by deal, raising equity from accredited investors for each specific transaction rather than managing a committed fund. Target businesses typically have $1M–$10M in EBITDA with enterprise values of $5M–$75M.

- Investing alongside family offices or making direct sponsor connections is a great option, but they do require more of a network and a deeper understanding of private equity transactions and generally the ability to add outside value apart from capital.

- Co-investment platforms like CapitalPad are the most accessible entry point, offering curated independent sponsor syndicates and deal flow with organized diligence materials and minimums as low as $25K.

- 68% of independent sponsors who completed exits returned 3x MOIC or more to investors, according to the Citrin Cooperman 2025 Independent Sponsor Report.

- Three main access channels exist: co-investment platforms (lowest barrier to entry), family office networks (relationship-dependent), and direct sponsor relationships (highest minimums, best long-term deal flow).

- Capital is illiquid for 3–7 years. Independent sponsor investments have no secondary market in most cases. Investors should only allocate capital they will not need during the hold period.

Table of Contents

- What Is Independent Sponsor Investing?

- How Independent Sponsor Deals Work

- What Returns Can Investors Expect?

- How Independent Sponsor Deals Differ from Search Funds and PE Funds

- Key Criteria for Evaluating Access Channels

- Comparison of Access Channels

- How to Invest in Independent Sponsor Deals

- Which Channel Is Right for You?

- Frequently Asked Questions

- How to Get Started Investing in Independent Sponsor Deals

What Is Independent Sponsor Investing?

An independent sponsor is a deal professional (typically with prior private equity, investment banking, or operating experience) who sources and acquires businesses without a committed fund behind them. Instead of deploying capital from a pre-raised fund, independent sponsors raise equity capital on a deal-by-deal basis from accredited investors, family offices, and institutional co-investors after identifying a specific acquisition target.

For investors, this structure creates a fundamentally different dynamic than traditional private equity. Rather than committing capital to a blind pool deployed at a fund manager’s discretion, investors evaluate a specific business, a specific sponsor, and a specific set of deal terms before deciding whether to participate. Each deal is a discrete investment decision.

Independent sponsor deals occupy the lower middle market, typically targeting established businesses with $1M to $10M in EBITDA and enterprise values ranging from roughly $5M to $75M. These are operating businesses with real revenue, existing customers, and often decades of operating history. The businesses being acquired are not startups or speculative ventures. This distinction matters for risk profile.

The asset class has grown substantially over the past decade but has historically been difficult to access without existing relationships in the sponsor community. Co-investment platforms have emerged to solve this access problem, providing structured deal flow to accredited investors who may not have pre-existing sponsor or family office connections. According to the McGuireWoods Annual Independent Sponsor Survey, the independent sponsor model has become a recognized and established segment of private equity, with a growing population of active sponsors, capital providers, and professional intermediaries operating in the space.

How Independent Sponsor Deals Work

Understanding the mechanics of a typical independent sponsor transaction helps investors evaluate opportunities more accurately.

Deal Sourcing: Sponsors identify acquisition targets through proprietary outreach, broker relationships, and industry networks. Many sponsors focus on specific industries or geographies where they have established expertise and deal flow advantages.

Acquisition Financing: The capital structure of a typical independent sponsor deal combines multiple sources. Senior debt (usually from commercial banks, SBIC funds, or private credit lenders) typically covers 40–60% of the purchase price. Seller financing is common, particularly in smaller transactions, with sellers rolling a portion of the purchase price into a subordinated note. Investor equity fills the remainder, representing the capital raise that accredited investors participate in.

Equity Raises: Equity raises in independent sponsor transactions typically range from $2M to $15M, although larger deals can require more. Investors receive equity ownership in a holding company or SPV structured specifically for the acquisition.

Sponsor Economics: Independent sponsors earn through two mechanisms. Management fees are modest annual fees paid from the operating company’s revenue that cover ongoing oversight responsibilities. The more significant incentive is the promote, or carried interest, which entitles the sponsor to a share of investment profits above defined return thresholds. Promote structures vary, but performance hurdles are common, with sponsor carry increasing at waterfall thresholds tied to investor returns. The McGuireWoods Independent Sponsor Survey publishes current market terms annually and is the most reliable public reference for benchmarking fee and carry structures.

Hold Period and Exit: Independent sponsors typically target hold periods of 3 to 7 years. Exits occur through strategic sales to industry buyers, acquisitions by larger private equity funds, or recapitalizations. Investors receive their returns at exit, including any accrued preferred return and their share of appreciation.

What Returns Can Investors Expect?

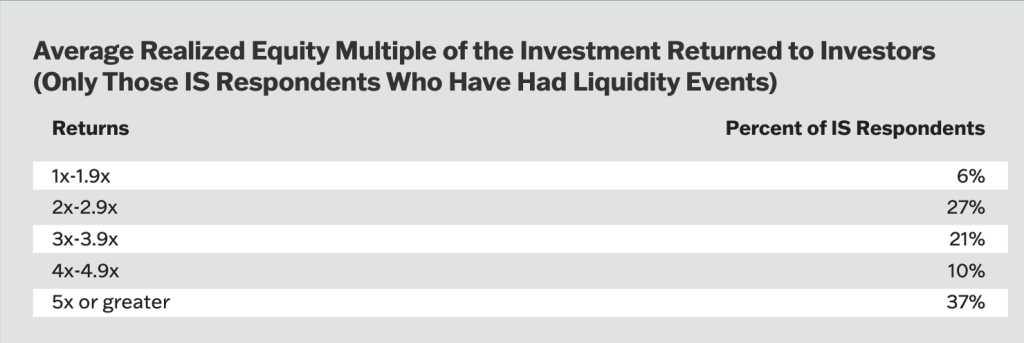

Return data for independent sponsor transactions has historically been difficult to aggregate. The Citrin Cooperman 2025 Independent Sponsor Report provides the most comprehensive public dataset currently available.

According to that report, 68% of independent sponsors who had completed liquidity events returned 3x MOIC or more to investors. More than 30% of completed transactions returned 5x MOIC or greater.

Source: Citrin Cooperman 2025 Independent Sponsor Report

These figures reflect completed transactions (deals that reached exit) and do not include unrealized or ongoing investments. Investors should interpret return data accordingly. As with all private equity, returns are highly dependent on deal selection, sponsor capability, and entry valuation discipline.

Investors should pay particular attention to how a sponsor’s promote and waterfall thresholds affect net returns. A 3x gross return may translate to a meaningfully different net figure depending on management fees, preferred return hurdles, and the carry split above each threshold. Understand the full waterfall before committing capital.

How Independent Sponsor Deals Differ from Search Funds and Traditional PE Funds

Versus Traditional PE Funds: Traditional private equity funds raise committed capital upfront and deploy it at the fund manager’s discretion across multiple investments over a defined period. Investors commit to a blind pool with no deal-by-deal approval rights. Independent sponsor deals invert this structure. Investors evaluate and approve each individual transaction before committing capital, retaining significantly more control over what they own.

Versus Search Funds: Search funds are a related but distinct model, most common among MBA graduates acquiring a single business to operate full-time. Search funds typically use SBA financing, which can cover up to 90% of the purchase price but requires a personal guarantee from the searcher. This financing constraint limits search fund acquisitions to smaller, simpler businesses and effectively limits searchers to one deal at a time.

Independent sponsors, by contrast, typically finance acquisitions through commercial lenders and private credit sources for debt, turn to sophisticated capital providers for equity investments, access larger businesses, and retain professional management rather than operating the business personally. Experienced independent sponsors often maintain a portfolio of three to four platform companies simultaneously, holding board seats and advisory roles in each while leaving day-to-day operations to existing management teams.

Key Criteria for Evaluating Access Channels

Before choosing an access channel, investors should evaluate their own position across several dimensions. These criteria shape which approach is practical and productive.

1. Accredited Investor Status

Independent sponsor deals are private securities offerings restricted to accredited investors under SEC Regulation D. Investors must meet income ($200K+ individually, $300K+ jointly for two consecutive years) or net worth ($1M+ excluding primary residence) thresholds and verify their accredited status before investing in deals.

2. Minimum Check Size

Minimum investment thresholds vary significantly across channels. Co-investment platforms and syndicates may allow participation at $25K–$50K per deal. Investing directly in a sponsor as a meaningful capital partner generally requires $750K or more per deal. Investors should be realistic about what minimum check sizes they can commit to consistently, since sponsors and platforms take allocation reliability seriously.

3. Time Horizon and Liquidity Tolerance

Independent sponsor investments are illiquid. Capital is locked up until an exit event, which typically occurs 3 to 7 years after the acquisition closes. Investors who may need access to their capital within that window should not participate. There is no secondary market for these positions in most cases.

4. Relationship Capital and Network Position

Some access channels require warm introductions, existing relationships with family offices, or a track record within the independent sponsor ecosystem. Investors who are earlier in their network development need channels that provide structured access to deal flow without relying on pre-existing relationships.

5. Bandwidth for Due Diligence

Evaluating an independent sponsor deal requires reviewing financials, assessing the business and industry, understanding the capital structure, evaluating the sponsor’s background and track record, and analyzing deal terms. This is not passive investing. Investors with limited time or expertise for diligence may benefit from platforms that provide curated, pre-screened deal flow with organized materials.

6. Desired Depth of Involvement

Some investors want to be passive equity participants. Others want governance rights, board observer seats, or the ability to contribute operational or industry expertise. The channel through which you access deals largely determines how much influence you can realistically negotiate.

Comparison of Access Channels

| Access Channel | Best For | Typical Minimum | Relationship Required | Deal Volume | Not Ideal For |

|---|---|---|---|---|---|

| Co-investment platforms (e.g., CapitalPad) | New investors; efficient, structured access | $25K–$100K | No | Moderate, curated | Investors seeking governance rights or bespoke terms |

| Family office connections | Investors with existing relationships; anchor-sized checks | $250K–$1M+ | Yes | Variable | Investors without warm introductions or established credibility |

| Direct sponsor relationships | Investors deploying $750K+ per deal; seeking proprietary deal flow | $750K+ | Yes | Low initially, high long-term | Investors seeking immediate deal flow |

How to Invest in Independent Sponsor Deals

For most accredited investors, a co-investment platform is the most practical starting point for investing in independent sponsor deals. Platforms provide immediate, structured access to active transactions without requiring pre-existing relationships with sponsors or family offices. The other two channels — family office networks and direct sponsor relationships — offer advantages for investors with larger check sizes and established networks, but require significantly more time and relationship capital to access.

1. Co-Investment Platforms (Recommended Starting Point)

Best For: Individual accredited investors seeking structured, efficient access to independent sponsor deals, particularly those newer to the asset class or without established relationships in the sponsor community.

Co-investment platforms aggregate active independent sponsor deals and present them to accredited investors in a standardized, reviewable format. For investors, the primary value is straightforward: you can see real transactions without needing pre-existing relationships with sponsors. This solves the access problem that has historically been the primary obstacle to entering this asset class.

CapitalPad

CapitalPad is a deal-by-deal co-investment private equity platform built specifically for independent sponsor transactions. Accredited investors join the network, review curated deal flow, and allocate selectively based on their own criteria. CapitalPad is in essence a private equity syndicate that pools investors together to complete transactions.

Deals on CapitalPad center on established, cash-flowing lower middle market businesses. Each opportunity is presented with organized diligence materials (business financials, deal terms, capital structure, and sponsor background) so investors can evaluate transactions without having to construct the information set from scratch.

Unlike generalist platforms that mix venture, real estate, and private equity deals, CapitalPad focuses exclusively on independent sponsor acquisitions in the lower middle market private equity space. This specialization means deeper screening of sponsors and deal structures, which matters in a space where sponsor quality is the single largest variable in deal outcomes.

CapitalPad operates a selective, curated model rather than a high-volume open-submission platform. The practical effect is that deal quality on the platform tends to be higher than less-screened alternatives, although deal volume is more limited as a result.

Key Features:

- Deal-by-deal participation with no blind pool commitments

- Curated deal flow with baseline quality screening

- Organized diligence packages for each transaction

- Defined economics with fees, carry, and ownership structures disclosed upfront

- Minimum investments as low as $25K on select deals

- Accessible to accredited investors without prior private equity experience

- Focused specifically on independent sponsor transactions (not a generalist platform)

Best For: Accredited investors who want structured access to independent sponsor deals, are earlier in their private markets experience, or do not yet have established sponsor relationships. Also well-suited for investors who want to evaluate the asset class in practice before committing significant capital.

Not Ideal For: Investors seeking large allocation sizes, governance rights, or the ability to negotiate bespoke deal terms. Co-investment platforms generally offer standardized terms with limited room for investor-level customization.

How it compares: Relative to building direct sponsor relationships, CapitalPad provides immediate access without a multi-year relationship-building phase. Relative to family office connections, it requires no warm introduction and enables lower minimum investments. The trade-off is reduced deal exclusivity and less influence over terms compared to investors deploying larger checks through direct channels.

Other Co-Investment Platforms

The independent sponsor co-investment space includes other operators, primarily generalist private equity platforms that feature lower middle market acquisitions alongside venture and real estate deals. These broader platforms typically offer higher deal volume but less curation and less specialization in the independent sponsor model.

Best For: Investors who want exposure across multiple private equity sub-categories simultaneously.

Not Ideal For: Investors specifically focused on independent sponsor transactions, where sponsor experience and deal structure knowledge matters significantly.

2. Family Office Connections

Best For: Investors with existing relationships in family office circles, or those willing to invest multi-year effort in building them. Best suited for investors targeting larger check sizes and repeat deal flow from established sponsors.

A number of independent sponsor deals never reach co-investment platforms, especially those from experienced sponsors with track records. These sponsors tend to raise entirely within their existing capital network: a small group of family offices and trusted co-investors who have worked with the sponsor before. These networks operate on reputation and relationship, not open access.

Family offices frequently act as anchor investors and receive deal flow, and they occasionally share it with others in their network. Access is referral-based. Sponsors prioritize investors who have demonstrated reliability, responding quickly, following through on commitments, and engaging constructively during diligence and post-close.

How deals surface through family office connections:

- Direct outreach from sponsors to known capital partners

- Introductions through other family offices or co-investors

- Participation in private investor groups organized around repeat deal flow

Best For: Investors with established introductions to family office networks, capacity for larger check sizes, and patience to build relationships over time before deal flow materializes.

Not Ideal For: Investors without warm introductions into these circles, or those seeking immediate deal flow. Access is slow to build and difficult to manufacture without genuine relationship capital.

3. Direct Relationships with Independent Sponsors

Best For: Investors seeking proprietary deal flow and long-term partnership with a small number of high-quality sponsors, and who are in a position to deploy $750K or more per deal.

The best independent sponsor deals often never leave the sponsor’s existing investor base. Sponsors raise capital from investors they already know, trust, and have worked with successfully. Fundraising from a familiar investor base is faster, more predictable, and less disruptive to the acquisition process than outreach to new capital providers. Direct capital partners at this level are typically expected to deploy $750K or more per deal, with many relationships involving significantly larger checks.

Building direct relationships requires a longer time horizon than access through a platform, and investors who pursue this channel typically start laying groundwork well before any deal is on the table. Sponsors gravitate toward investors who provide genuine value: introductions to acquisition targets, relevant industry insight, and constructive engagement during diligence. That kind of contribution builds the goodwill that earns a place on the short list when deals emerge. Sponsors remember investors who made their work easier, not just those who wrote checks.

How direct relationships form:

- Prior co-investments with the sponsor through any channel

- Referrals from other investors or professional advisors

- Introductions through shared industry or professional networks

- Conference attendance and follow-through (the fantastic McGuireWoods event and similar events are active networking venues)

Once established, these relationships offer early visibility into deals before formal capital raises begin, flexibility to discuss allocation size and terms, and access to follow-on and add-on transactions as sponsors grow their portfolios.

Best For: Investors deploying $750K+ per deal with relevant industry expertise or professional networks that sponsors find valuable, and a long time horizon before expecting consistent deal flow.

Not Ideal For: Investors seeking immediate deal access, or those whose desired check size is below the $750K threshold that direct sponsor relationships typically require.

Which Channel Is Right for You?

Different investor profiles call for different access strategies. The table below maps investor situations to recommended starting points.

| Investor Profile | Recommended Starting Point | Why |

|---|---|---|

| New to independent sponsor investing | CapitalPad | Immediate structured access; no relationship prerequisites; low minimums to evaluate the asset class in practice |

| Experienced private markets investor with family office connections | Family office networks | Higher deal quality on average; repeat access once trust is established |

| Investor deploying $750K+ per deal | Direct sponsor relationships | Direct access to proprietary deal flow; flexibility on terms and allocation size |

| High-net-worth investor not yet deploying $750K+ per deal | Co-investment platform + family office relationship development | Use platforms for near-term deal flow while building broader connections in parallel |

| Investor with limited time for active diligence | Co-investment platform | Curated deal flow with organized materials reduces research burden |

Frequently Asked Questions

How do I start investing in independent sponsor deals?

The most straightforward way to start is to join a co-investment platform that focuses on independent sponsor transactions, such as CapitalPad. These platforms are typically free to join for accredited investors and provide curated deal flow with organized diligence materials, allowing you to review live transactions and allocate selectively with minimums as low as $25K per deal. No prior private equity experience or sponsor relationships are required.

How much capital do you need to invest in an independent sponsor deal?

Minimum check sizes vary by channel and by deal. Co-investment platforms like CapitalPad typically allow participation starting at $25K on select transactions. Family office networks generally involve larger commitments, often $250K–$1M or more. Direct sponsor relationships typically require $750K or more per deal.

What is the difference between an independent sponsor and a private equity fund?

Independent sponsors raise capital deal by deal rather than managing a committed fund. Investors can evaluate each opportunity independently rather than committing to a blind pool. The trade-off is that investors must conduct diligence on each individual transaction rather than relying on a fund manager’s judgment across a portfolio.

Are independent sponsor investments risky?

All private equity investments carry risk. Independent sponsor transactions face execution risk (can the sponsor close and integrate the business effectively?), market risk (does the industry environment support the business plan?), and financial risk (can the business support its debt load?). Failure rates tend to be substantially lower than venture capital because the target businesses are established and cash-flowing rather than speculative startups. But underperformance is possible, and thorough diligence on the sponsor, business fundamentals, and deal structure is essential.

Do independent sponsor investments pay dividends or distributions?

Some independent sponsor-acquired businesses generate sufficient cash flow to support periodic distributions to equity investors during the hold period. Many do not, with value accumulating primarily at exit. Investors should review the specific operating plan and financial projections for each deal to understand what interim distributions, if any, are projected.

Do I need to be an accredited investor?

Yes. Independent sponsor deals are private securities offerings available only to accredited investors under SEC Regulation D. Accredited investor status requires meeting income thresholds ($200K+ individually or $300K+ jointly for two consecutive years) or net worth thresholds ($1M+ excluding primary residence). You will need to verify your accredited status before accessing deals through any platform or channel.

How to Get Started Investing in Independent Sponsor Deals

For investors entering the asset class for the first time, a co-investment platform like CapitalPad is the logical starting point. Most are free to join for accredited investors and allow you to review live transactions before committing any capital. The goal early on is to develop judgment about what strong deals and capable sponsors look like in practice.

In parallel, begin building relationships before you need them. Identify sponsors whose backgrounds and deal focus align with your criteria and introduce yourself directly. Independent sponsor conferences (particularly the McGuireWoods Independent Sponsor Conference) are among the most efficient venues for meeting active sponsors, family offices, and other capital providers in a single setting.

Be patient and selective. Deal flow in this asset class is uneven, arriving in waves rather than on a fixed schedule. Resist the instinct to deploy quickly into the first available opportunity. Review broadly, commit narrowly, and invest in becoming known as a reliable and disciplined capital partner. The groundwork you lay in the first year compounds steadily and pays real dividends in years three and four.

For benchmarking independent sponsor fee and carry structures, see the McGuireWoods Annual Independent Sponsor Survey. For return data, see the Citrin Cooperman 2025 Independent Sponsor Report.

Updated April 03, 2026.