A couple of days ago I was browsing along on The Twitter and stumbled across a tweet and article by DHH talking about something that really caught my attention.

“Why isn’t there a market for selling a minority stake of your profitable tech company to people who’d be happy to be paid back in distributions and dividends, rather than capital gains? It seems like a glaring gap in the market.”

Welp, as you can see he pretty much summed up exactly what we’re up to at Smash.vc. Although admittedly, he had something with a little bit bigger scale in mind, similar to the deal he and Jason did with Jeff Bezos during Basecamp’s early days. So there I was, pretty happy about just getting some external validation about the benefits of our business model from DHH when low and behold a brand new tweet popped up.

Well well Travis, it’s obviously your lucky day. You couldn’t have gotten a better advertisement if you tried. DHH is one of the largest voices in the “alternatives to VC” space.

Seeing as I’m currently visiting Taipei, I was just about to hop into the hotels super-soft bed for a much needed sleep. This tweet changed that plan. I had some responding to do. What we’re doing at Smash makes all the sense in the world to me, but I know that to many people it may seem counter-intuitive. “How do you make money?”, “What is the required growth rate of the companies you invest in?”, “What’s the catch?“, etc.

As a result of these questions that I keep getting, I’d love to take a couple of paragraphs to explain why I believe this business model might make perfect sense for many investors AND founders. I believe it can be a truly win-win scenario. The below is specific to Smash, but I believe the answers should be roughly the same for all investors playing in this field.

So here we go…

FAQ of the Smash.vc Business Model

How do we make money (i.e. get a return on our investment)?

When Smash “invests”, we are simply buying common shares of the company from the founder(s). So we get rewarded in the same way the founder does, ideally through dividends (profits) distributed over the longterm.

What are the benefits for founders?

The main benefit to most founders is just simply “taking chips off the table”. It’s a way for founders to have a partial-exit, put some extra cash in the bank account to feel more secure, but yet not having to sell the entire company right now (or ever). This is not an investment into the company, it is buying shares directly from founders, with the proceeds going into their personal accounts not into the company account.

I know the emotions around this all too well. In my most successful business to date my co-founder and I had a life-changing offer on the table. We knew that the company could be so much more, we loved the team, and we were good at what we did. But we were also scared that something would happen to the business that would wipe us out and leave us with nothing. So we sold, which was still great and all, but we know in retrospect that we left A LOT of money behind, and we had to watch our baby not live up to its full potential with the new owners.

I wish something like Smash could have existed to let us take chips off the table and keep on running. Having some experienced guidance would have really helped too. We didn’t know what we didn’t know.

This is why I believe this model can be a true win-win for all parties involved.

Do you expect a liquidity event?

Nope. In the words of Warren Buffett “Our favorite holding period is forever“. I would actually say that I’m exit-agnostic. If a founder wants to sell the company eventually, great, we will help them in any way we can. If the founder wants to just hold forever and distribute profits, even better. We’ll support you either way.

How does this work with a fund?

No idea, because we are not a fund. All money invested into these deals comes straight from mine and any co-investors pockets. As Taleb would say, we have “skin in the game“. On top of that though, it just didn’t sound very fun to setup, figure out, and manage a fund in a way where incentives were properly aligned with all parties.

I know there is some way to structure this as a fund, Brent Beshore for example, (who is a joy to follow) has a permanent-capital-ish fund setup to buy and hold companies for an indefinite time horizon. Would love to hear more from him on it.

How is this different from a VC?

I’m not going to get on an “anti-vc” rant, because I’m not anti-vc. It works for many companies, I’m just all about giving founders more options, opening up opportunities to more entrepreneurs, and doing it all while creating good opportunities for Smash.

I’m not going to get on an “anti-vc” rant, because I’m not anti-vc. It works for many companies, I’m just all about giving founders more options, opening up opportunities to more entrepreneurs, and doing it all while creating good opportunities for Smash.

Some key differences:

- We actually expect to get returns from dividends instead of liquidity events. If liquidity events happen, then that’s cool too.

- Growth is not all that important. I’m just fine holding a small business that stays small (more on that below)

- We don’t need massive exits for the economics to make sense. Owning a piece of a company making a healthy living is good to me.

- Smash can play at a much much smaller scale than Venture. With VC you invest with valuations starting in the millions because the upside is so huge if “it works”. Try getting a lifestyle business valued at $5MM pre-product. It just doesn’t work like that. But that’s ok with us, lifestyle businesses sound great.

What’s the catch?

What are the economics of it?

First off, disclosure that this is specific to the playing field that we invest in. Our ideal check size is $100k-$200k (mayyyybe up to $1MM if we bring in co-investors on a deal). Our pockets only run so deep right now. For us, we don’t really care about the ownership percentage we buy in a business, so we could put in $200k for 5% of a $4MM business, or $200k for 49% of a $400k business.

As for how to value a business, I really hate to say “it depends”, but it really does. I’ll give some ideas though. When you hear of companies getting bought up by the Google’s and Facebook’s in strategic acquisitions you hear crazy multiples like 10x revenue. Not profit, revenue.

The vast majority of companies simply don’t fit into this mold though. Certainly not smaller businesses, certainly not lifestyle businesses. For these types of businesses you can generally value the business at a multiple of SDE (seller’s discretionary earnings) or EBITA.

To make it simple, we’ll just say a business would be valued just like it was being sold in its entirety with a business brokerage (Empire Flippers, FEinternational, QuietLight Brokerage, etc). And to make it even more simple, it’ll be valued at a multiple of “profit”. Usually in the neighborhood of 3x annual profit. This goes down for some businesses (with increased risk, less diverse earnings, weak traffic sources, slow to no growth, etc) and goes up with others (recurring revenue, scalability, high growth, high margins, not capital intensive, etc).

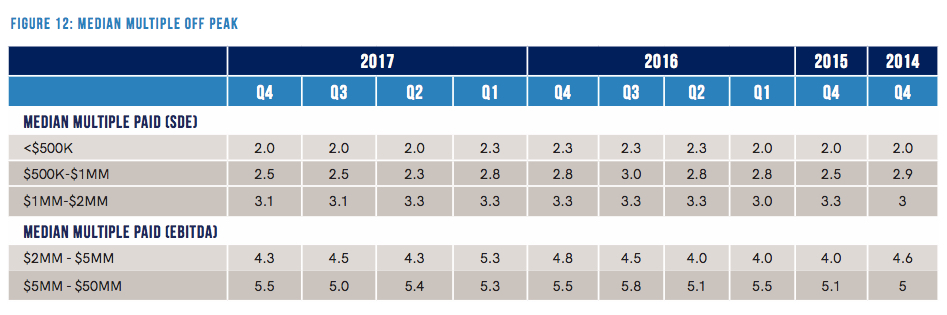

Here’s a handy chart.

Source: Pepperdine Private Capital Market’s Market Pulse Survey via Adventur.es (< this is a good post btw)

Source: Pepperdine Private Capital Market’s Market Pulse Survey via Adventur.es (< this is a good post btw)

Source:

Source: For more traditional “startups”, the businesses are usually valued more on growth instead of profitability. This is why many startups are playing that crazy game. Nothing wrong with it as long as you know the game you’re playing. But if it’s the game you’re playing then it’s growth at all costs. High risk high reward vs lower risk lower reward. To me any many others though, “low reward” can still be an incredible quality of life and more money than you could ever need, just might not be in the 3-comma club.

What about growth?

Smash is not growth at all costs. But even more than that, we don’t even necessarily need to see significant growth in a business. Being steady is ok. Steady can work for us, because we are really good at growing online businesses. We have a separate growth agency, and a lot of in-house talent. So usually (but not always) if we invest my team will be rolling up our sleeves and doing growth work ourselves.

But, even if our growth team isn’t a good fit, it can still work.

I don’t have profit yet, are you interested?

Most likely not, but there are a few others who would be a much better fit. Investors like TinySeed, Indie.vc and Earnest Capital (I’m actually an LP in Tiny and Indie) are setup to help fund and assist companies who need a little funding but are coming from a profits-first bootstrapped mindset.